Nomi’s note: All eyes are on the Federal Reserve right now. The market wants to know whether it’s going to reel in its easy-money policy, like it claims it will… or if it’s bluffing.

This is nothing new. In my days as a senior strategist at Lehman Brothers, we were always ready to trade on the Fed’s moves. We had a little ritual for it, which I shared with you yesterday…

Below, my colleague Eoin Treacy sheds light on this story from a different angle. He shows you what it means for the dollar… and how the Fed’s push to bring down inflation could play out in the stock market. Read on…

We are in a new interest rate hiking cycle.

Federal Reserve chairman, Jerome Powell, was very clear about that last week. His statements about raising interest rates and quashing inflation shocked investors.

The most important thing is the Fed gave up giving forward guidance. What do I mean by that?

Before last week, it prioritized being predictable. It gave clear signals about where it believed interest rates would go.

Now, it just doesn’t know.

Last week, Powell committed the Fed to being nimble. That implies it will adjust policy in response to inflation.

He also said that inflation has gotten worse since the beginning of the year.

That means the Fed will raise rates by 0.25% when it meets again in March.

And it implies that it will raise rates faster unless inflation starts coming back down pretty soon.

Now, it’s worth remembering that talking about raising rates and doing it are two different things.

As our editor Nomi Prins put it yesterday, the Fed serves two masters – the economy and the stock market.

It looks at the stock market as a barometer for the success of its policies. If stocks continue to weaken, the Fed will not be able to raise rates as much as it would like.

Still, we are likely to see some rate hikes this year – even if it’s not as many as the markets expect. And this new policy means some assets will do much better than others.

Below, I’ll share one group of stocks that can weather rising rates. But first, some background…

New Strong Dollar Policy

No other major developed market has been as clear about its intentions as the U.S. has.

And this has consequences for the dollar – and dollar-based assets.

Currencies don’t trade in isolation. The prices we see are always relative to each other.

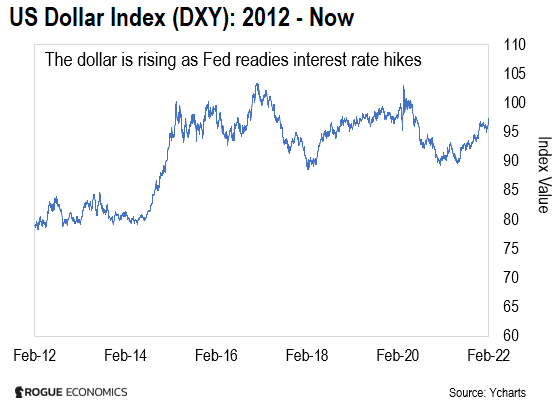

So when pundits talk about a strong dollar, they are usually talking about the Dollar Index.

The Dollar Index is a basket of currencies. The big weightings are 57.6% euro, 13.6% Japanese yen, and 11.9% British pound.

None of these central banks are talking about aggressively raising rates, like the Fed is.

In fact, when the European Central Bank (ECB) and the Bank of Japan (BoJ) tried to raise rates after 2012, they failed. Every time they tried to raise rates their economies experienced deflation. They will lag now too.

The difference in interest rates between currencies influences how they trade.

As you can see in the chart below, the dollar is rising against these currencies. That’s because the Fed is talking about raising rates faster than everyone else.

That will continue until other central banks are also forced to raise rates.

A Boon for the Bond Market

By keeping a lid on rising yields, the Fed can keep the U.S. government’s borrowing costs lower for longer.

That’s great news because the government’s debt total increased by 25% during the pandemic.

But that’s not the only benefit of low interest rates.

As the dollar rises, U.S. assets become more attractive to foreign investors. That’s very important for the bond market.

Ten-year Treasuries yield almost 1.8%. Meanwhile, German government bonds yield negative 0.05%.

If the dollar keeps rising against the euro, European investors will flock to the U.S. bond market.

The same is true for most other markets.

One of the biggest jumps the dollar posted was against the Chinese renminbi. That’s going to make dollar assets more attractive to Chinese investors, too.

What This Means for Your Money

Now, as I mentioned earlier, the Fed is going to have a hard time raising rates as quickly as the market expects. Nomi wrote about this in more detail yesterday.

See, the Fed has distorted how the bond and stock markets function. This is at the heart of the market disconnect Nomi speaks about.

The Fed might wish to raise rates aggressively, but it is still at the mercy of the financial markets.

That said, we can still expect some rate hikes this year. What does that mean for investors?

Right now, stocks that went public recently are among the market’s worst performers. They don’t handle rising rates well.

Fitness bike maker Peloton (PTON) and virtual communication company Zoom Video Communications (ZM) are two examples.

Many value stocks, on the other hand, are well-positioned to weather higher rates.

As Nomi pointed out in the January 18 dispatch, the best-in-class companies tread a path between growth and value.

These are companies with strong cashflows, established margins and pricing power. They shine when inflation picks up.

That’s why they have turned to outperformance.

The Vanguard Value ETF (VTV) bounced last week while the wider market faltered. It’s going to be a lot more popular if the Fed is serious about fighting inflation.

All the best,

Eoin Treacy

Contributing Editor, Inside Wall Street with Nomi Prins

Like what you’re reading? Send your thoughts to [email protected].