Welcome to our Friday mailbag edition!

Every week, we receive some great questions from your fellow readers. And every Friday, I answer as many as I can.

The dollar is in the spotlight once again this week. It’s been a common theme in these mailbags. And as you’ll see in my answers, there’s good reason for that.

So let’s get to them…

Why is the dollar continuing to be strong, and what might change that in the near term?

– Richard S.

Thanks for your question, Richard! You’re right about the dollar.

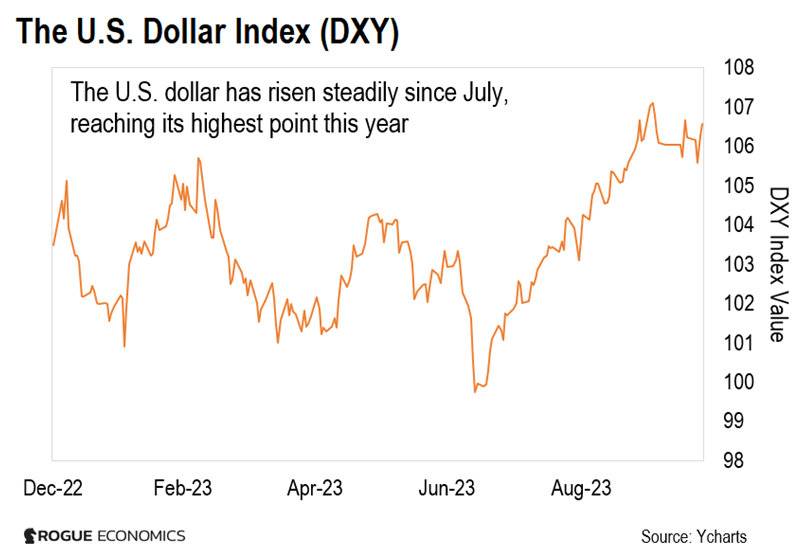

Relative to other currencies, the dollar is stronger than it’s been in two decades. It has rallied about 7% since July, to its highest point this year.

You can see that in the chart below. It shows the U.S. Dollar Index (DXY), which tracks the value of a dollar against a basket of foreign currencies…

The dollar is up even more than that if we compare it to other individual currencies. Since the start of the year, it’s up double digits against currencies like the Japanese yen.

One of the biggest drivers of the dollar’s strength right now is the Federal Reserve. Since last year, the Fed hiked interest rates at the fastest pace in 40 years. This brought rates to a 22-year high.

That impacts the dollar because, when interest rates rise, people get a higher return on their savings. This tends to attract foreign investment in the country with high rates. And that increases the demand for – and value of – that country’s currency.

That’s exactly what’s happening right now with the dollar. And, until the Fed starts cutting rates, I expect the dollar to get stronger against most other currencies.

That’s also because of the dollar’s appeal as a safe haven during times of turmoil. And there is so much of that right now worldwide. If history is a guide, this will also continue to drive more demand for the dollar.

Remember, much of what gives the U.S. dollar its value is the extent to which it is used as the world’s reserve currency.

Today, central banks hold about 58% of their foreign reserves in U.S. dollars. The rest is in euros (20%), British pounds (4.9%), Japanese yen (5.5%), and Chinese yuan (2.6%).

What that means is that the dollar is still king. It’s the dominant reserve currency by almost three times the next largest currency, the euro.

This makes the markets confident that no matter how bad things might get, the U.S. will continue to support the dollar and back its national debt payments.

Now, the U.S. Dollar Index I mentioned earlier still has a way to go to break its previous high of 164.72. It set that record in 1985.

I’m hoping we won’t see geopolitical tensions rise to the levels we experienced back then. But, either way, those tensions are in the spotlight, and the Fed isn’t backing down from high interest rates just yet.

That should keep pushing the dollar up, relative to most other currencies, in the next few months.

To be clear, none of that means that your purchasing power is getting stronger if you live in America. Yesterday, I showed you why the opposite is true.

Between our skyrocketing debt… and the high-interest payments the government must pay to avoid a default… the dollars in your pocket are losing value fast.

The dollar has lost 96% of its value since 1913. That’s the year a group of wealthy bankers pushed Washington to create the Federal Reserve.

That downward spiral won’t end as long as the Fed keeps making bad decisions that hurt Main Street America. I’m not holding my breath for that.

That’s one of the reasons why I keep advocating in these pages for everyone to own some hard assets. But it’s not the only one.

Which brings us to our next question…

I find your Weekly Mailbag extremely helpful in understanding our financial situation. My simple question is: Where should I stash my cash, especially if a CBDC becomes a reality? I do not support CBDCs because I do not want the government to spy on me. I want to maintain my freedom.

I’m a retired naval officer and federal (not political) senior executive. I try to take my family to see the world as much as I can afford it. I envy your ability to travel the world! I need to maintain some cash so I can do that. Thank you for your time and expertise!

– Edwin C.

Thank you for your kind words, Edwin. I admire your desire to show your family the world.

You bring up an important question. Before I answer it, let me give other readers some context.

Every day, our government gets closer to adopting a central bank digital currency (CBDC) and transforming our monetary system.

In September 2022, the White House even issued a framework to research the effects of a CBDC. It’s the White House’s first comprehensive framework for what they call “responsible development of digital assets.”

In it, the Biden administration “encourages the Federal Reserve to continue its ongoing CBDC research, experimentation, and evaluation.” It lays out seven main areas for this research.

(You can read it in full on the White House’s website, here.)

Here’s the thing about the White House issuing that framework. It means there have been and will continue to be conversations between the White House and the Fed about a CBDC.

The Fed got a step closer to an all-digital dollar when it launched its FedNow payments system this summer. As you know, I consider FedNow a necessary precursor for a CBDC.

In that sense, the U.S. is riding a global trend:

-

98 central banks are in the process of planning the digitalization of their currency.

-

More than 80% of global banks are exploring digital currency.

-

And overall, 130 countries are already exploring digital currencies.

Now, you mentioned that you’re worried about maintaining your freedom.

The reality is, the faster we move toward a CBDC, the easier it will be for the government to monitor – and in some cases, even curtail – our financial choices.

For example, it will give the government more power to compile data on how and where we spend our money. That would take away what little freedom we have left to decide what personal information we share and what we keep private.

A CBDC could even be programmed so that you can only spend it if you meet certain requirements.

This means that, if you do something the government doesn’t like, it could fine you. Or even worse, at the push of a button, it could turn off your ability to transact.

And this isn’t just speculation. That’s exactly what happened in Canada last year when the government froze hundreds of bank accounts connected to protesters.

In a negative interest rate scenario, as a CBDC holder, you might have to pay a small fee to the Fed. It’s like a mini tax on your savings, with the Fed taking a chunk out of your digital wallet regularly.

These are just a few examples highlighting how much easier it will be for the government to take away your financial power and freedom when all legal tender becomes digital.

As for the best place to stash cash, that’s a decision only you can make.

But what I advocate for all of my readers is to ensure your portfolio has a mix of cash outside of the banking system.

Some might choose to keep at least part of that cash in a safe.

Hard assets that can be used as currency are also a good option. I’m a big fan of gold and Bitcoin for this purpose.

I released a video report with more on this. In it, I give details on my No. 1 gold stock – and the best way to buy and store your Bitcoin. You can watch that here.

If we have an account directly with the Fed – in other words, a digital wallet – why will we also need an account with a traditional bank?

Will this change make the local and regional banks redundant and hence obsolete? And if so, why would they go along with this plan? Without deposits, they can’t make loans or extend credit.

– Gary B.

Hi, Gary! That’s a great question.

I’ve written a lot about how the Fed would benefit from the advent of the digital dollar in these pages.

As a government body overseeing the monetary system, it would gain enhanced control and oversight over people’s transactions. So much so that the Fed could have unprecedented financial control over our lives.

A digital dollar would also enable the Fed to fabricate money out of thin air. That’s because it’s easier – and faster – to create a CBDC electronically than a fiat currency.

That said, you’re right that a CBDC could disrupt the traditional role of banks. So why would they be in favor of such a thing?

For one, a CBDC will allow traditional banks to remain relevant in an ever-more digital financial landscape. By embracing CBDCs, banks can position themselves as key players in the evolving digital currency ecosystem.

As such, they’d remain proactive, rather than reactive, and at the forefront of financial innovation.

Plus, banks and the Fed both see the digital dollar as a way to level the playing field in the payments ecosystem. Or so they say, at least.

What we do know for sure is that this is where the real money is. For some context, the global digital payments market size will be valued at $9.5 trillion in 2023. Almost 22% of that is in North America.

And it’s estimated to reach roughly $15 trillion by 2027. That’s a 56% growth in just four years.

For perspective, the GDP of the entire European Union in 2022 was about $16 trillion. So, the payments market size is set to be roughly on the same scale as the EU’s total economic output.

That’s why banks have been itching for a shot at the payments game. They’re trying to keep up with other payment options like PayPal, Venmo, and Zelle.

For banks, it’s a chance to step up, earn trust, and show they’re “dependable financial players” in what they try to paint as the “increasingly unstable digital world.”

Finally, with an all-digital dollar on the horizon, banks have a chance to gain new business prospects.

Collaborating with the Fed and offering digital payment services and innovative financial products is a plus for traditional banks. They can use this to unlock new avenues for revenue growth.

So, yes, there are many reasons for banks to be on the same page as the Fed when it comes to the digital dollar.

In fact, the big banks have long been gearing up for the eventual rollout of a digital dollar.

As far back as 2017, a consortium including finance giants like Citigroup and JPMorgan Chase initiated a real-time payments network operated by The Clearing House, known as the RTP Network.

This network processed a total of 135 million transactions worth about $60 billion during 2022.

Now, the idea behind real-time payment networks is to help lay the technical groundwork and foster a culture of digital currency acceptance. While also giving regulators a taste of what’s to come.

But this summer, the financial elites, spearheaded by the Fed, took it to a whole new level. Heavy hitters like JPMorgan, Wells Fargo, Bank of America, and Citigroup rallied behind the initiative.

This lays the foundation of an all-digital dollar. It will be the first step towards embracing a new kind of currency.

This is yet another reason to own gold and Bitcoin as part of a balanced portfolio. With the rollout of an all-digital dollar, it’s good to have some capital outside of the traditional financial system.

And that’s all for this week’s mailbag. Thanks again to everyone who wrote in!

I do my best to respond to as many of your questions and comments as I can each Friday.

If I didn’t get to your question this week, please write me at [email protected]. Just remember, I can’t give personal investment advice.

Happy investing… and have a fantastic weekend!

Regards,

Nomi Prins

Editor, Inside Wall Street with Nomi Prins