THIS ESSAY WAS ORIGINALLY

PUBLISHED OCTOBER 7, 2016, IN STANSBERRY DIGEST

Today, we’re taking on a big economic mystery…

Doesn’t sound exciting, does it? Well, what you’re going to learn below will be responsible for earning some investors trillions in profit over the next five years.

Investors who don’t understand these concepts are going to get wiped out. What’s the concept? It’s the answer to the following questions…

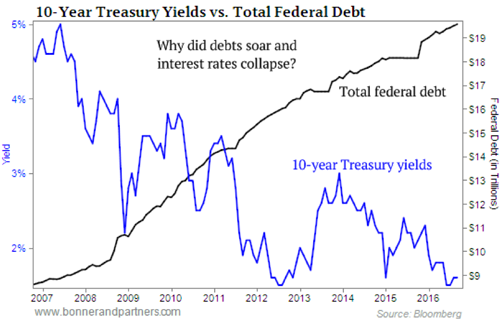

Given a more than 100% increase in federal debt and federal debt securities over the past few years, why haven’t bond prices fallen and why haven’t interest rates risen? Where is all of the inflation that should have occurred?

As you know, bond prices not only didn’t fall (causing interest rates to rise), they continued to hit new all-time highs (sending rates to new all-time lows). In many places (covering around 25% of global GDP), bond prices rose so much that interest rates went negative, something most people thought was simply impossible.

|

Of course, federal debt levels aren’t the only thing that has exploded…

Student debt, auto lending, U.S. corporations, and, perhaps the biggest debt bubble of all, foreign corporations.

In the U.S., corporate obligations are at all-time highs, relative to GDP (a little more than 45%). But in China, they’re even crazier: Corporate obligations have soared in the past eight years from virtually nothing to more than 120% of GDP. The corporate debt and real estate bubble in China is probably the largest the world has even seen. (Imagine working out that problem in a nation without the rule of law or a tradition of recognizing property rights.)

In total, the International Monetary Fund says that global debt is now equal to 225% of global GDP, up from about 200% just a decade ago.

Just about every economist in the world would have told you that massive increases to credit and money supply and the resulting huge expansion of consumption would have set off massive inflation, or, at the very least, much, much higher interest rates.

So… why didn’t it happen?

It’s the most important economic mystery of our lives. And the answer is finally coming into firm relief, thanks to a lot of new, fascinating economic research from major economists… all of which is teaching us something most of us would have simply called common sense: Socialism doesn’t work.

My tutor in these ideas is Dr. Lacy Hunt. He’s a Ph.D. and a practicing economist who helps direct $4 billion of investments at Hoisington Management in Austin, Texas.

Hoisington has taken a unique investment position for the last 25 years. It has put its clients into virtually nothing other than long-duration, zero-coupon U.S. Treasury bonds, which capitalize all interest payments, compounding them for 20 or 30 years.

No other investment vehicle in the world is better suited for lower inflation or, even better, deflation.

And Dr. Hunt has ridden this trend for longer than anyone else. He didn’t even blink when the Fed and every other central bank started printing stupendous amounts of money.

How did he know? What did he see in the global economy that nobody else (including yours truly) saw?

What’s the secret to his analysis?

At Jim Grant’s biannual get-together in New York this week, I found out.

Dr. Hunt explained it in great detail over the course of an hour. Don’t worry… I know you’re not interested. And I can boil it down into one simple concept that I know you’ll grasp immediately.

The problem revolves around a simple idea that economists call a "multiplier"…

They’re referring to the effect new capital has when injected into an economy. Ever since the 1920s and the days of John Maynard Keynes, economists everywhere have assumed that government borrowing and spending would produce a positive multiplier for the economy. They’ve thought of the government’s spending as "priming the pump." For example, if the government borrows money to build new roads, then private industry would be spurred to build new houses along the roads and build new businesses to serve those houses, etc.

That’s the theory. But does it actually happen in practice? That’s where a whole slew of new research comes in.

As it turns out, there is a multiplier effect associated with government spending. But based on empirical studies, it’s actually negative. That is, rather than spurring growth, there’s a strong correlation between more government borrowing and more government spending with less economic growth.

If you want to dive deeper into this puzzle, here are a few of the most important new studies…

-

Blanchard, Olivier, and Roberto Perotti, "An Empirical Characterization of the Dynamic Effects of Changes in Government Spending and Taxes on Output," Quarterly Journal of Economics (2008)

-

Ilzetzki, Ethan, Enrique G. Mendoza, and Carlos A. Vegh Gramont, "How Big (Small?) Are Fiscal Multipliers?" International Monetary Fund working paper (2011)

-

Dupor, William, and Rodrigo Guerrero, "Does Government Spending Create Jobs, Even During Recessions?" The Regional Economist (2016)

-

Perotti and Roberto, "Estimating the Effects of Fiscal Policy in OECD Countries," IGIER working paper 276 (2004)

Assuming you don’t want to spend a week reading economic research, let me simply tell you what Dr. Hunt and these other researchers have discovered. It won’t surprise you…

Governments are generally really bad investors…

Much of the capital they borrow and invest is wasted. And as debt-to-GDP levels surpass around 80% of GDP, the real problems begin. The research above suggests that when debt-to-GDP levels stay above 90% for more than five years, the resulting damage to economic growth is particularly severe.

Worst of all, changes to the multiplier of government spending are non-linear. The multiplier doesn’t just get a little bit worse as debts and spending increase. It falls of a cliff as debts mount.

Or, in plain English, the more money governments borrow and spend, the worse the impact is on economic growth and wealth creation.

The data show that our economy is likely to experience big declines in GDP growth as our government continues to borrow more and more and spend more and more in an effort to reverse the declining economy.

That will hurt overall productivity, corporate profits, industrial production, employment, and consumer spending – all with increasing severity as the magnitude and duration of the debt is extended.

We’ve already seen these troubling data points occur over the past 24 months. Government borrowing and spending is literally digging our financial graves.

The harder they dig, the worse it’s going to get…

As for interest rates, the factors I’ve described should be more than enough to keep interest rates low, but it gets worse…

By adding the impact of quantitative easing (where the government prints money to buy bonds and manipulate interest rates lower), they’re magnifying the impact of this financial repression.

According to these studies, that’s going to have an unintended consequence: much lower consumer spending.

Think about this for a minute. The government has basically sold $10 trillion in debt over the last few years.

If that debt was trading freely in the market – and hadn’t been bought by central banks around the world – what would the interest rate be? Economic theory and more than a hundred years of data tell us that interest rates should be roughly equal to annual GDP growth plus a nominal return above the inflation rate. If growth is 2.5% and inflation is 2%, you should see short-term government bonds trading around 4.5%, with longer-dated bonds trading a little higher, say 6%.

Now, think about how much income would be generated by all of that new debt. Just looking at the new debt (6% of $10 trillion) would see an extra $600 billion a year sent into private hands.

Looking at the total federal debt ($20 trillion), that’s $1.2 trillion a year of capital sent into private hands – if the public owned these bonds and bills and if interest rates were allowed to rise.

That’s a significant amount of income for the private sector. But what happens when interest rates are manipulated to nothing and most of the debt is held by central banks or government "trust" funds?

That’s taking capital away from private hands (consumption and investment) and putting it into government programs (waste, malinvestment, and disincentives to gainful employment).

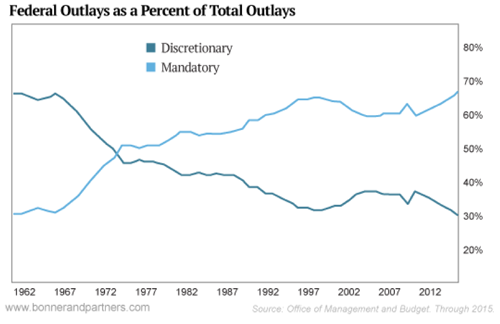

Just think about what the government spends money on.

Our government (and all the other major Western democracies) has embraced the kind of social spending programs that bankrupt every nation that adopts them.

|

The chart above shows "mandatory spending" (aka government transfer payments) versus discretionary spending, which is everything else. Our government is no longer building bridges and enforcing contracts. It’s simply taking money from Peter to pay Paul. And as you’d expect, that kind of economic activity (aka stealing) has a negative multiplier. Taking lots and lots of capital from productive hands and giving it to unproductive hands might meet political goals, but it’s not good for the economy.

Ready for this shocking conclusion? Socialism doesn’t work. And manipulating interest rates makes it a lot worse.

One last point…

Corporations are borrowing record amounts of money…

Despite slower economic growth and artificially low interest rates, these companies are taking on huge amounts of debt.

And they’re not spending the money on new production. They’re simply refinancing old loans and buying back stock. Over the last year, total corporate bond issuance totaled $833 billion. But net business investment was negative $64 billion. That’s not going to increase economic activity. It only increases leverage. And risk.

Think about this… Artificially low interest rates restrict growth, limit consumer spending, and encourage individuals and corporations to borrow far too much money. Imagine what’s going to happen when we go into a recession again.

We’re seeing record debt at the corporate level, the government level, the consumer level (auto loans), and an entire generation (students) encumbered by massive debt.

Do you think those conditions are going to lead to calm, cool, and rational policy decisions? Do you think those conditions are going to be good for our banking system? Do you think that’s going to make us less aggressive with our foreign policy? (It’s Mexico’s fault!) Do you think our political leaders are going to wake up and realize that it’s their policies that have put us in this mess?

No way.

They’re going to keep "doubling down" until the whole thing blows up.

I’m 100% certain we’re going to enter another recession next year…

I’ve been writing about the warning signs for a long time – falling industrial production, declining trade, falling corporate profits, and rising corporate defaults. And I told you that employment would roll over next. It has. The jobs report today showed that unemployment ticked up to 5%. The employment situation has been getting steadily weaker for the last year.

That’s the last nail in the coffin. Next year is going to be ugly for stocks. But it will be even worse for corporate bonds.

In 2017, we’ll see the first maturities on the huge amount of junk bonds that were issued in the record issuance cycle between 2010 and 2015.

Roughly $125 billion will be due. The default rate across the sector will approach 10%. It will be much more difficult, and maybe impossible, for companies to refinance these obligations. And it will continue to get worse and worse. In 2018, another $250 billion will come due. In 2019, another $350 billion. And that’s before two years of $400 billion or more in junk matures in 2020 and 2021.

If we’re in a recession next year… look out. All of these debts will be seen as unfinanceable. The bond prices of highly leveraged companies will seriously collapse as these liquidity problems spread. As for stocks, the damage to share prices will be much worse.

The fact is, most of these loans should have never been made. These companies are vastly overleveraged. And their financial condition, as a group, hasn’t improved since 2010… It has gotten worse. The huge bubble we’ve seen in junk bonds has financed massive overcapacity, where these companies simply can’t generate enough income to pay back their loans. A reckoning is coming – and it’s long overdue.

Unfortunately, small, junk-rated companies aren’t the only ones who will have a big problem…

Historically, "investment grade" meant that a corporation was extremely unlikely to ever default, regardless of the economic circumstances. The overall investment-grade default rate is usually just above zero during a recession. However, the lowest-rated "tranche" of investment-grade debt (BBB) would typically see a few defaults. In the default cycle between 1998 and 2002, a little more than 1% of these bonds defaulted. But… BBB isn’t what it used to be.

We know from our analysis of corporate credit in Stansberry’s Credit Opportunities that a lot of BBB credit is just wishful thinking.

A good example of a weak BBB credit is Devon Energy (DVN). We know the company well. Back in 2014, we essentially begged Devon to prepare for a big fall in the price of oil by selling its Canadian oil sands assets to pare down its debt and invest in higher-quality assets, like the Eagle Ford Shale.

The company never bothered to reply to our concerns. Around six months later, just about everything we warned them would happen did happen. Now, its oil sands assets are an anchor around the company’s throat. Meanwhile, it’s carrying more than $12 billion in debt, which is equal to 267% of its equity.

Today, Devon is a highly levered oil and gas business that routinely operates with negative cash flows. (Last year’s tally was negative $290 million.) Incredibly, in our minds, despite the obvious risks to this individual balance sheet and the historic booms and busts of the domestic energy industry, Devon’s benchmark bonds are only paying 3.4% and the company is rated BBB.

How can a company be considered "investment grade" if a one-level credit downgrade could leave it unable to access the capital markets? After all, in periods of credit stress, junk-bond issuance disappears. And selling assets won’t repay these debts… The company is far too encumbered.

There are dozens and dozens of companies like Devon. Maybe hundreds.

How bad is the situation, really?

Historically, the BBB tranche of the investment-grade market made up a tiny portion of the total investment-grade market. But that has changed since 2009. As companies added debt in this cycle, more and more of them have been downgraded into BBB – just one step above junk-bond credits. Where 10 years ago only 14% of investment-grade bonds were BBB-rated, today more than 30% of the investment-grade market is BBB-rated. In other words, "investment grade" just doesn’t mean what it used to.

That’s why even though annual default rates on investment-grade bonds have historically been low, we suspect that the coming default cycle is going to be much, much worse. I expect we’ll see annual default rates on BBB debt of at least 3%, with cumulative defaults reaching close to 15%. Keep in mind, almost $2 trillion worth of BBB-rated "investment grade" debt is outstanding. Losses like the kind I expect during the next cycle could result in more than $500 billion in total defaults. And that’s just the defaults from the "investment grade" debt.

I’ve been warning about the coming credit cycle for about a year…

So far, I’ve been pretty much on the mark. Default rates keep creeping higher and higher. Economic conditions are getting weaker and weaker. What’s coming in 2018 and 2019 will be the biggest economic storm of our lives. It’s going to wipe out a lot of people – unemployment will go way over 10%. And more than $1 trillion worth of bonds will default. This is absolutely going to happen, because while the government can buy all the bonds it wants, it can’t make them pay.

This situation doesn’t have to be a disaster for you, though. Don’t think of it a crisis. Think of it as a reckoning. The foolish and spendthrift are going to learn a lesson. And the wise and patient will reap their fair reward. That’s why I call what’s coming "the greatest legal transfer of wealth in history." It’s going to be an incredible show.

Want a front-row seat?

Then please join us in my latest research project, Stansberry’s Big Trade. If you know that a record amount of corporate debt is going to default, what should you do? We decided to build our own database of virtually every U.S. corporate obligation. We look at 40,000 separate securities every month and assign our own credit ratings to between 3,000 and 4,000 issues.

So far, we’ve focused on buying short-dated credits that offer us big yields and that we’re certain won’t default in Stansberry’s Credit Opportunities. So far, we’ve made about 40% annualized gains and haven’t seen a single loss. Our hard work is already paying off for the subscribers of this publication. But we can do a lot more with this data…

Our plan is to spend the next five years or so predicting corporate defaults. We want to figure out who is going to default and when. That’s not hard to do, but it doesn’t create much value for investors if a company’s existing rating (and share price) reflects its dire financial condition.

What we’re going to do is a little different… and potentially a lot more valuable. We’re looking for weak credit where there’s still tremendous equity value and an undeserved rating. We’ve done that work over the last month and put together our list. It’s called "The Dirty Thirty." I went over the stats on this group of companies last week. It’s incredible. As a group, these stocks…

-

Carry more than $300 billion in debt,

-

Produced negative free cash flow of $40 billion over the last decade, and

-

Are still worth more than $192 billion in market capitalization.

These companies are going to put a huge dent into the net worth of millions of Americans…

Believe me, I’m aware of the dangers investors in these companies’ stocks and bonds face. But I can’t change it. I can only try to help my subscribers survive and prosper.

Our strategy will be to buy long-dated put options on these firms. Then we just have to wait for credit conditions to deteriorate, which we know they will, as access to additional capital is restricted for weak credits like these. When that happens, our put options could end up being worth 10 to 20 times more than when we paid for them. We don’t even need these companies to file for bankruptcy. We just need the market’s perception of their access to additional capital to change. That alone will send these stock prices much, much lower.

It should go without saying that this type of investing (speculating, really) isn’t for most people. We understand. But if you have a lot of exposure to these risks, it makes a lot of sense to allocate 5% or 10% of your portfolio into these trades. I believe it will be possible to make 10 times your initial capital on these trades as a whole. That’s how you can turn this situation from a tragedy into your greatest triumph.

As I hope you can tell, I’ve personally spent a lot of time on this project and I’ll continue to do so for the next several years. This isn’t going to be a "quick hit" trend. I expect these trends to play out over the next five years. You might think that means you have a lot of time to prepare, but you would be dead wrong. As soon as these risks are common knowledge, our opportunity will be gone.

We have to establish our put positions before other investors realize these risks. We have to use the super-low volatility in the stock market right now to our best advantage. So I’m urging you not to wait on this. Please. Nothing would be worse than seeing all of this coming and not being able to hedge yourself or speculate for profit.

Stansberry’s Big Trade could easily make you more money than you’ve ever made in your life. Most people, I believe, can see the value we’re offering. I hope you’ll be one of them.

Regards,

Porter Stansberry

Editor’s Note: We’re seeing unprecedented warning signs in credit markets all around the world…

The global scale of these problems means the coming crisis – what Porter has called "the greatest legal transfer of wealth in history" – will be truly historic.

Folks who don’t see what’s coming could be wiped out… while those who prepare now could set themselves up to earn a fortune, as much as 10–20x their money, as the inevitable bust plays out.

This is why Porter is hosting a live presentation on Wednesday, November 16, at 8 p.m. ET to explain it all… what he’s calling his biggest trade yet.

He’ll tell you exactly what happens next and what you need to do to prepare. If you still haven’t reserved your spot yet, we urge you to do so now by clicking here.