Welcome to Inside Wall Street with Nomi Prins! It’s the only daily newsletter featuring the insights of Nomi Prins and her team of global experts. You’ll find all our issues here. And if you have questions or comments, shoot us a note anytime here or at [email protected].

I have only come out ahead with an insurance company once. And it taught me all I need to know about the corruption that lies at the heart of the industry…

A few years ago, after a small side-swipe accident, I was quoted $17,000 to fix a dent in my car that should have only cost $500.

If you’ve ever been in a situation like this, chances are you don’t have a great relationship with insurance either.

But there’s one thing even I can’t deny, despite all my personal frustrations with insurance over the years…

The insurance business makes lots of money.

In today’s essay, I’ll show you how you can reap some of those profits. First, let’s look at what makes the insurance industry such a money machine.

Paying for Something You Can’t Afford to Use

It’s easy to see why the insurance industry is so lucrative…

The basic business model for insurance companies is to take in more in premiums than they pay out in claims. The margin between those two figures is their raw profit.

I constantly see ads on TV selling health insurance. They always talk about the low premiums, but they never talk about the $5,000-$10,000 deductible.

If you don’t get health insurance through your job, that deductible is a big hurdle. It means you pay for health insurance, but you can’t afford to use it.

And of course, there are also years that you pay your insurance premium, but you don’t need to make a claim. In 2019, just 5% of insured homes had a claim, for example.

So all those premiums – from people who can’t afford to make a claim and those who don’t need to – go straight to the insurance company’s bottom line.

Globally, the insurance industry wrote $6.3 trillion worth of premiums in 2020. Of those premiums, $2.5 trillion were written in the U.S.

That makes the U.S. the biggest insurance market in the world, accounting for about 40% of the global insurance market.

Now, the U.S. insurance market has more than doubled over the last 10 years. You can see the steady growth in the table below…

Global and U.S. Insurance Industry 2010 – 2020

|

Year |

Total global premiums |

Total premiums written in the U.S. ($US trillions) |

|

2010 |

4.3 |

1.1 |

|

2011 |

4.5 |

1.2 |

|

2012 |

4.6 |

1.2 |

|

2013 |

4.5 |

1.2 |

|

2014 |

4.7 |

1.2 |

|

2015 |

4.6 |

1.3 |

|

2016 |

4.6 |

1.3 |

|

2017 |

5.7 |

1.3 |

|

2018 |

6.1 |

1.4 |

|

2019 |

6.2 |

2.4 |

|

2020 |

6.2 |

2.5 |

Source: Insurance Information Institute

And according to Insurance Business America, global insurance premiums are set to grow to $10 trillion by the end of the decade.

That means the U.S. insurance market could be worth up to $4 trillion by 2030. That’s 60% higher than where it is today.

Time to Let Insurance Companies Pay You

Insurance might be a dirty business, but at its core, it’s about reducing the number of risks we are exposed to. That’s why it has grown so much over the last decade… and will continue to grow in the future.

That internal conflict we feel drives to the heart of the disconnect our editor, Nomi Prins, has identified between the financial markets and the real economy.

We know that risk exists. We don’t want to believe it will affect us, but we pay to protect ourselves anyway. We do that even though it means sacrificing spending on areas of our lives that would make us happier.

Whether it’s health, life, auto, weather, or home risks, each of these trends represents a growth market for the insurance sector. People will always seek to protect themselves, their families, and their businesses from the risks around them.

So how do you take advantage of this?

One of the easiest ways is through an exchange-traded fund (ETF). An ETF allows you to own some of the best names in the sector with just one click of your mouse.

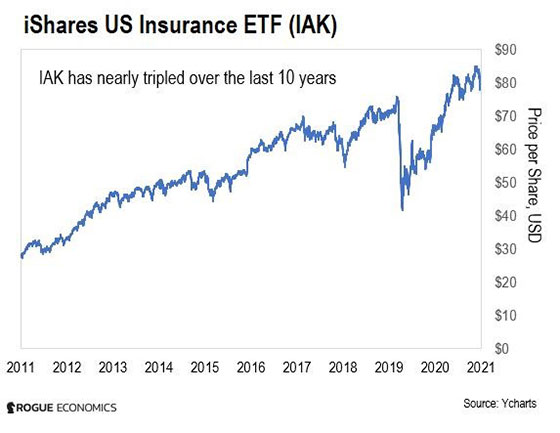

My favorite insurance fund is the iShares U.S. Insurance ETF (IAK). It tracks a basket of the biggest names in the U.S. insurance business, including Progressive, Prudential, and Allstate.

Take a look at its chart below…

As you can see, the fund is up roughly 200% in the last 10 years. And, with the U.S. insurance industry estimated to grow from $2.5 trillion to about $4 trillion by 2030, I expect IAK to keep trending higher.

That makes the iShares U.S. Insurance ETF (IAK) a good bet today if you want to make the insurance industry work for you.

Plus, it also pays a dividend of 2.3%. That’s higher than the S&P 500’s yield of 1.2% at the time of writing.

And by the way, about the car involved in the incident I mentioned up top… My insurance company wanted to total it. But I paid a guy $500 to knock out the dent.

65,000 miles later, it’s still going strong. My daughter is taking driving lessons. That Porsche Cayenne will be her first vehicle.

All the best,

Eoin Treacy

Contributing Editor, Inside Wall Street with Nomi Prins

Note From Rogue Economics’ Senior Managing Editor

Last week at Rogue Economics, we welcomed our new editor, Nomi Prins. Nomi is a best-selling author and financial journalist. But once, she was a Wall Street insider.

Nomi worked as a managing director at Goldman Sachs… ran the international analytics group as a senior managing director at Bear Stearns in London… and was a strategist at Lehman Brothers and an analyst at the Chase Manhattan Bank.

Now, Nomi brings her keen understanding of the world of money to Rogue Economics. In these pages, Nomi will show you why she left her career as a global investment banker… and set out to demystify the world of money.

She will also put you on the right side of a disconnect she sees between the markets and the real economy. She’ll do this with help from her team of global experts – including 20-year gold and natural resources investor and trader Eoin Treacy… and longtime metals, tech, and cryptocurrency investor Laurynas Vegys.

Of course, if you prefer not to get daily insights from Nomi and her team, you can unsubscribe at any time. You’ll find a link to do so at the bottom of every Inside Wall Street with Nomi Prins email.

Best regards,

Maria Bonaventura

Senior Managing Editor, Rogue Economics

P.S. As always, let us know what you think – good or bad. Write us at [email protected].